We solve all your doubts, so we are on the same page

We answer all your questions in straightforward language.

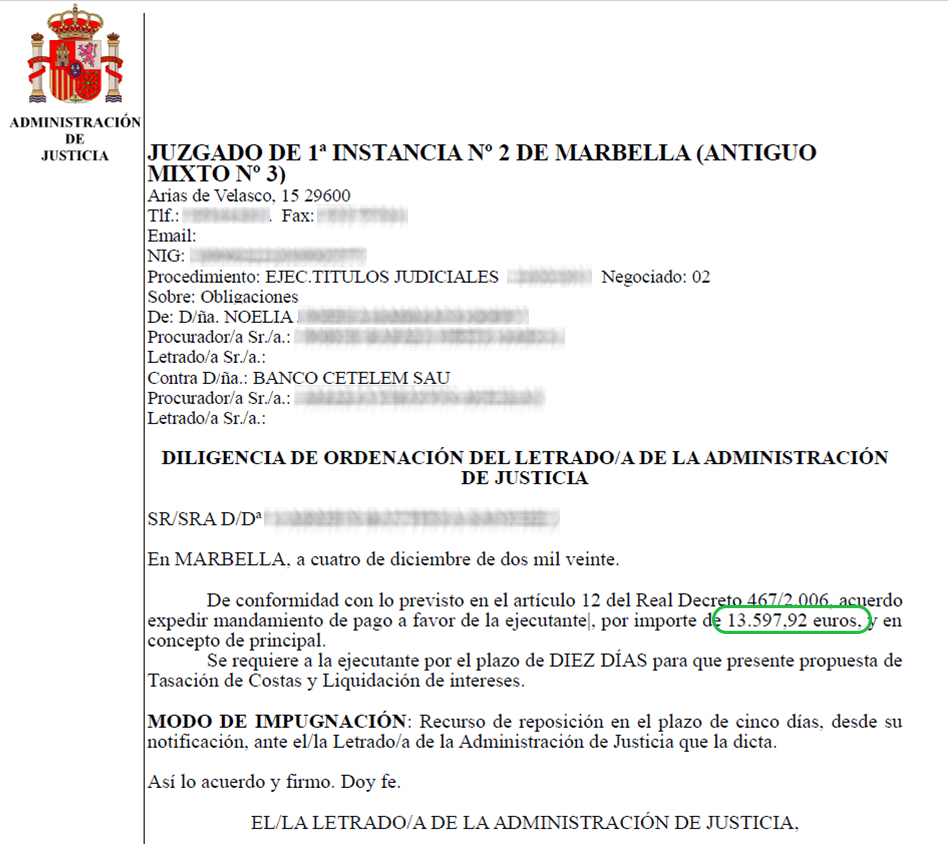

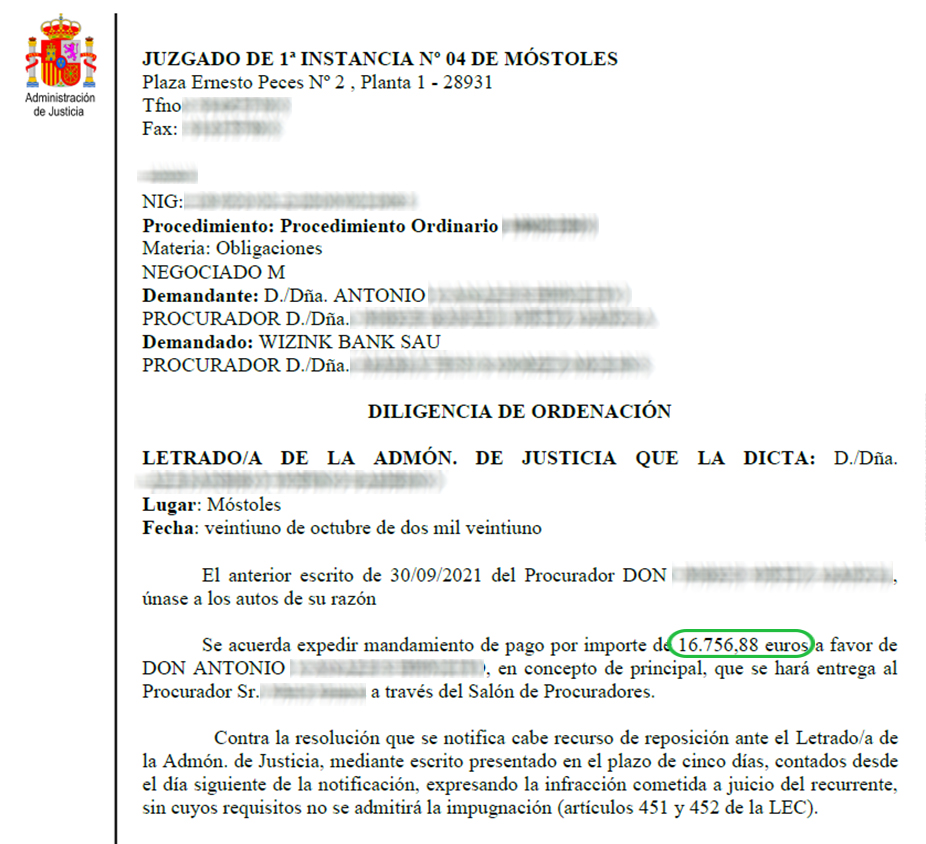

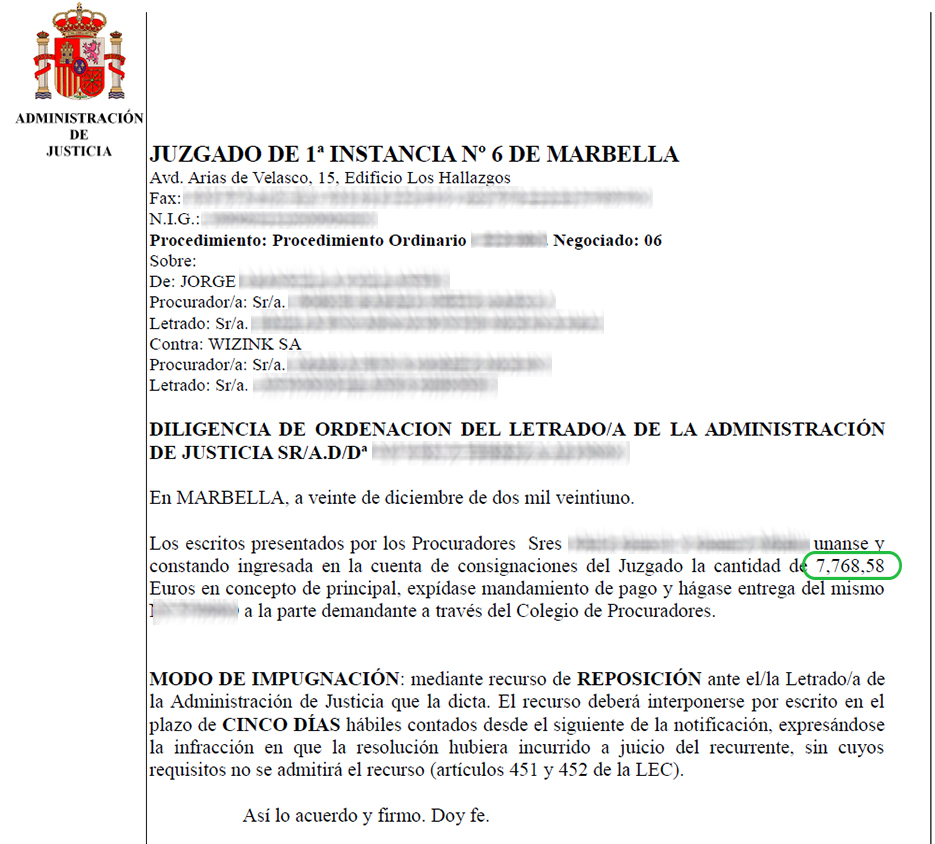

Indeed, we have had many successful outcomes on revolving credit card claims. Every client is different. The end result and amount recovered will depend on your situation. However, we can confirm that these claims have a high success rate. These are just some of the cases we have won:

You can find out by considering the following:

You can start your claim by filling in our form. It will take you less than 99 seconds.

To find out whether a credit card is subject to excessive interest rates, we must analyse the card’s details. There are certain revolving credit cards that seem eligible to claim: WiZink, revolving Cetelem, revolving Citibank, Cofidis, and the Carrefour Pass. Even so, every card should be examined.

These are just examples. It’s likely that one of the cards you have in your wallet is affected. Regardless of the financial institution. If you have accepted a very low fixed monthly fee, you may be paying excessive interest with each day that passes.

Mainly because you were charged excessive interest rates. The Spanish Supreme Court determined that an interest rate is considered excessive if it is significantly higher than average market interest rates. And this is what occurs with revolving credit cards.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

The goal is to cancel your revolving credit card contract and get reimbursed for the money you have overpaid. Since the interest rate is so high, we could be talking about significant amounts.

Your claim’s outcome will always depend on the individual circumstances of your case. Perhaps you haven’t paid back everything you have borrowed. In this case, it’s possible that there isn’t anything to be reimbursed by the financial institution.

What do we do if this is the case? We apply for the interest rate to be declared null and void. Therefore, you would no longer have to pay interest. This means you will pay less on the outstanding debt or, in other words, pay only the amount initially taken out. Interest-free.

So, if you’re in a similar situation, it is in your best interest to make a claim. This way, even if you don’t get any money back, you could still pay less and settle your debt. What’s more, with in99 you don’t have to pay a single euro upfront. We only get paid if your case is won. And if you’re worried about losing your case, we offer a legal fee insurance policy to cover the trial costs, in the unlikely event that you don’t win. Without any risks.

All you have to do is fill out our form with the information we ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

To make a claim on a revolving credit card, you’ll need certain supporting documents.

You will need to provide the contract you signed with the financial institution. If you don’t have your contract, another option is the amortisation table. This will show all the movements on your revolving credit card. This information will allow us to calculate how much you have overpaid.

You also have the option to send us your statements/settlements and we will take care of looking for the rest of the information for you. You can generally find these bank statements on your online account.

What can you do if you don’t have the contract or the amortisation table? In this case, you should contact the financial institution that offered you the line of credit and ask for a copy of both documents (your contract and amortisation table).

This request can be done both at the branch or online via their website.

When you manage to get in touch with them to ask for a copy of the documents, they will know that you need them to make a claim and they are likely to offer you a settlement. Our advice is to not sign any agreement, no matter how good it may seem. You may find yourself unknowingly giving up your right to take legal action and what they offered you was simply a reduced interest rate. This will then make it impossible for you to defend your rights as a consumer.

No, they’re two separate things. If you have a credit card and you purchase something, you pay the financial entity the amount due the following month. And the debt is paid off.

If you have a revolving credit card, you pay back the borrowed amounts in several instalments

with high interest rates. As a result, your debt is dragged out over time.

What if you get back more money than you expected?

It's normal to not be aware of everything you can claim. The same can be said regarding the protection of your interests. You can find out in under 99 seconds by answering a few simple questions.

I want to startIt's normal to not be aware of everything you can claim. The same can be said regarding the protection of your interests. You can find out in under 99 seconds by answering a few simple questions

{kind=link}

{kind=link}

{kind=link}